Many of your clients run their own businesses, but likely many of them are overwhelmed with the many different tax concepts involved, and how they can structure their business most effectively. An important concept for them to master in order to understand how to structure shareholders agreements and the value of corporate-owned insurance is the CDA or Capital Dividend Account.

How is the CDA Calculated?

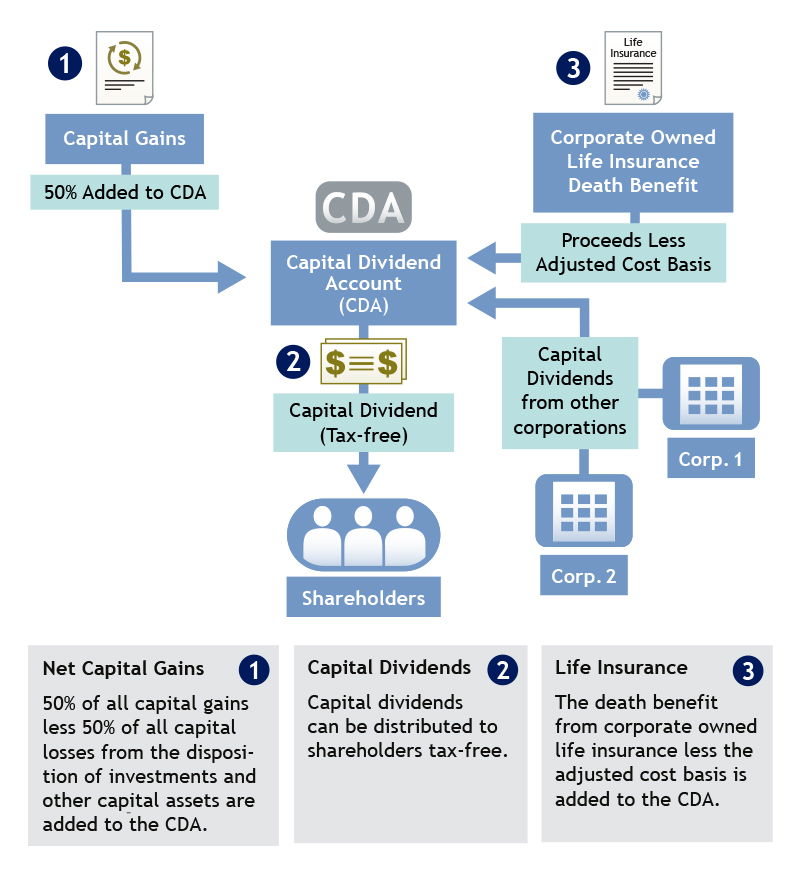

What exactly is the CDA they may ask? The CDA is a notional account that is calculated by your client (with their tax advisors), and can be verified with the CRA. Notional meaning that it is not a literal account that they transfer funds in and out of, but rather a cumulative calculation that simply let’s them know the amount of capital dividends their corporation can pay out.

Capital Dividend Account =

(Non – Taxable portion of Net Capital Gains)

+ (Capital Dividends from other Corporations or Trusts)

+ (Proceeds of Corporate Owned Life Insurance less the Adjusted Cost Basis)

– (Capital Dividends paid)

The equation above shows the general calculation of the CDA, though the infographic below is likely an easier way to process the information. In words though, 50% of capital gains are added to the CDA, however it’s important to note that 50% of capital losses are subtracted from the CDA as well. Proceeds from life insurance received by the corporation as the named beneficiary are also added to the CDA less the adjusted cost basis (ACB) of the policy. Capital dividends received from other corporations or trusts are also added to the CDA. And of course, any capital dividends declared are subtracted from the balance.

Using the CDA to Your Client’s Advantage

Understanding the CDA can be very beneficial for your client, especially when setting up a buy-sell agreement between shareholders, and when considering funding such agreements with corporate-owned life insurance. The CDA can be used as part of post mortem planning to reduce the tax liability on the death of a shareholder.

There are many advantages to having corporate versus personally owned life insurance. You can find an article about the benefits of corporate-owned insurance here.

Timing is Important

It’s also important to be aware of the potential pitfalls inherent in the CDA. Timing of the realization of capital losses and the payment of capital dividends is important. The overpayment of a capital dividend can result in steep tax penalties that can be avoided through careful tax planning. Clients should consult their tax advisors before deciding to pay a capital dividend.

By helping your clients understand the CDA and the benefits of careful planning using shareholders’ agreements, you can help them maximize their corporation’s value and secure their legacy.

SHARE the client article from The Link Between:

What’s in Your Capital Dividend Account?